Climate change is expected to alter hurricane activity, intensifying related risks across US coastal counties. And the Atlantic hurricane season begins from June 1st through November 30th in the North Atlantic Ocean, which causes devastating impacts on the millions of homes standing along the US coastlines- Texas to Maine. CoreLogic, one of the leading global property information, analytics and data-enabled solutions provider has released its 2023 Hurricane Risk Report.

The 2022 Atlantic Hurricane season killed at least 474 people and caused a loss of worth up to $165 billion, making it one of the costliest seasons of all time. According to NOAA, hurricane Ian had the highest price tag in the nation’s third-costliest year ever for disasters.

The report focusses on the evolving landscape of hurricane risk in the face of climate change. The report analyzes risks for single-family residences (SFRs) and multifamily residences (MFRs) along the U.S. Gulf and Atlantic Coasts.

The detailed report outlines:

- The quantified hurricane risk in the U.S.

- How many homes are in danger of damage

- The potential reconstruction costs, while taking inflation into account

- Risks by major metro areas

Tom Larsen, Senior Director for CoreLogic Insurance Solutions, stated, “CoreLogic remains committed to empowering the industry with reliable insights and innovative solutions that help safeguard people, businesses and communities from the escalating impacts of climate change. Insurers and lenders should adapt to these changes by deepening their understanding of property risk, embracing proactive loss prevention measures and collaborating with stakeholders across the industry to ensure long-term resilience.”

Highlights of the 2023 Hurricane Risk Report

The reports states that historically, the most severe hurricane-related damage has been concentrated in coastal regions adjacent to the Gulf of Mexico and the Atlantic Ocean. However, recent seasons have demonstrated that hurricane risk can – and likely will continue to – extend further inland, posing threats to millions more homes.

Evidence shows that climate change is impacting hurricane activity in the North Atlantic Ocean with a higher proportion of stronger (e.g., Category 3+), wetter hurricanes that have the potential to travel further inland before dissipating. The combined effects of these factors could significantly impact U.S. properties in future years, including those structures that were once considered out of reach of hurricane wind and flooding.

“Weather shocks are on the rise,” Ernst Rauch, chief climate scientist at Munich Re, told Reuters. “We can’t directly attribute any single severe weather event to climate change. But climate change has made weather extremes more likely.”

The report highlights:

National Implications

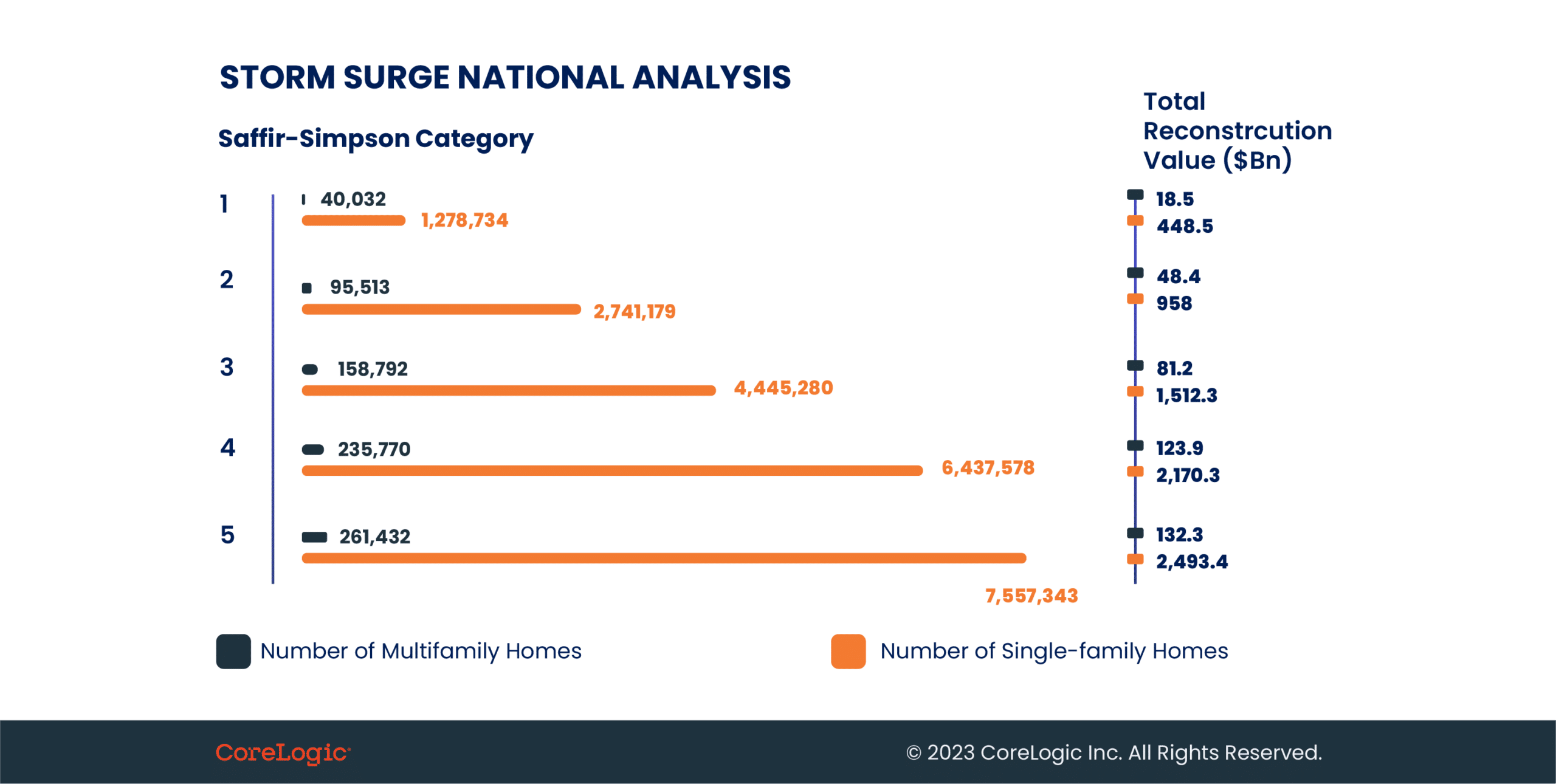

This year, CoreLogic has identified that more than 32 million single family residences (SFRs) and an additional one million multi-family residences (MFRs) are at moderate or more significant risk of sustaining damage from hurricane-force winds. This damage would have a combined reconstruction cost value (RCV) of $11.6 trillion. Approximately 7.8 million homes, with a combined RCV of $2.6 trillion, have direct or indirect coastal exposure, making them susceptible to storm surge flooding.

Metro Area Implications

CoreLogic’s 2023 Hurricane Risk Report has also identified major U.S. metros at greater risk for hurricane damage. More than 4.3 million SFRs and MFRs in the New York City metro area are at risk of hurricane-force winds. These properties, spanning New York City, Newark and Jersey City, equate to a combined RCV of $2.4 trillion at risk. Other major metro areas with substantial hurricane wind risk are the Houston-Woodlands-Sugar Land and Miami-Ft. Lauderdale-Pompano Beach areas have 2.1 million SFRs and MFRs, each, and a combined RCV of $649.8 and $585.0 billion, respectively.

Hurricane Projections by 2050

CoreLogic analyzed historical data, climate patterns and predictive models in conjunction with its property database and suite of climate change models to forecast the potential impacts of hurricanes on coastal and neighboring regions by mid-century.

Research suggests that, by the year 2050, more powerful storms, a rise in sea level and warmer atmospheric temperatures will give hurricanes a greater capacity to hold more moisture. Simultaneously, warmer sea surface temperatures give storms the fuel to penetrate further inland to locations previously shielded from consequential damage.

CoreLogic has found that the biggest increase in homes at risk of damage from hurricane-force winds are in the counties furthest from the coast, who had previously only experienced dissipated winds. However, by mid-century, homeowners may need to consider how to mitigate and recover from hurricane wind damage as storms travel further inland, exposing more homes to hurricane force winds. The 2023 Hurricane Risk Report further illustrates what these risks might look like, using the Houston-Galveston area as an example.

How CoreLogic made the report?

CoreLogic evaluated the storm surge and hurricane wind risk levels for both single-family (SFR) and multifamily (MFR) residences along the Gulf and Atlantic coasts for the 2023 hurricane season.

Over 7.5 million of these homes had direct or indirect coastal exposure and subsequent risk from coastal storm surge and damage from hurricanes. CoreLogic studies have indicated that up to 70% of the damages from flood to homes is uninsured.

Interestingly, the cost to repair (RCV) will be much more expensive this year, driven by changes in material costs, and construction costs specifically. This could have a much bigger economic impact despite the small changes in the number of homes.

Climate Change-induced Disaster

Climate change has increased the hurricane frequency thus causing sea-level rise, stronger winds, and higher rainfall rates. These have contributed to the increasingly damaging impact of hurricanes; exacerbate the risk of coastal and inland flooding and increase the risk of structural damage.

The insurance industry will see increased financial implications because wind damages are covered by standard homeowners insurance policies.

Flood insurance is widely adopted by homeowners within the Special Flood Hazard Areas designated by the Federal Emergency Management Agency (FEMA), but it is rarely purchased outside those zones. As a result, unsuspecting homeowners can be left with very little or zero protection in recovery from intensifying hurricane seasons.

With ocean temperatures rising, scientists predict that we should expect more frequent and destructive tropical cyclone activity. Homeowners and regional public agency leaders should recognize the need for more resilient city infrastructure and increased financial protection from catastrophe.