Advancing & Augmenting USD 1.4 Trillion Geospatial Market by 2030

Strategic public policy reforms, industry acceleration strategies, and innovations in the digital twin and metaverse paradigm to drive geospatial market growth post 2025.

GeoBuiz 22: Global Geospatial Industry Outlook Report

Geospatial industry is the next ‘Big Opportunity’ for technology companies both as an ‘advancing market in itself’ and ‘augmenting business processes’ of mainstream IT, Engineering and Autonomous industries. It would continue to provide accurate and rich foundation to data infrastructure and increasingly add the third dimension to ‘everything we do’. This will result in geospatial getting by default embedded in digital twin and metaverse, which will further impact how humans interact with digital and physical world in near real time. The technology leadership must look at geospatial market holistically as it is evolving to be a ‘process of insight’ as an outcome, while moving up the value chain in the field of reality capture in terms of coverage, context, themes, accuracy, and currency.

Data insight and knowledge economy

Data insight is at driving wheel of knowledge economy, penetrating and integrating across workflows and processes of every industry. And as every business gets more and more driven by insights, data would serve as oil to knowledge economy and shared economy business models, aimed at deriving greater efficiency, productivity, transparency, and compliance.

Geospatial infrastructure, which comprises of foundation data, positioning network, platform, standards, knowledge services, and policies, provides overarching framework and serves as the interface between government and commercial enterprises to work towards extending geospatial value chain and scalability of applications supporting development, governance, business, and security. Recognizing the growing value of geospatial knowledge infrastructure, there have been several initiatives towards public policy and industrial development worldwide, and the same has been laying the path for amplified growth by the year 2030 and beyond.

Source: GW Consulting

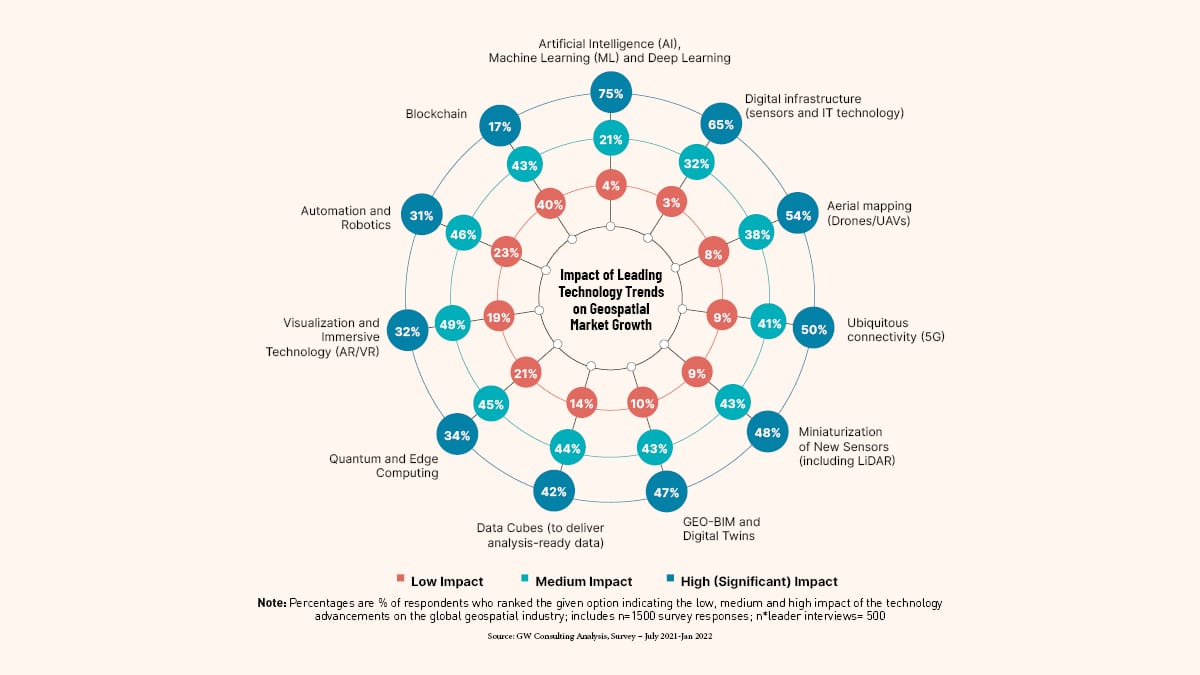

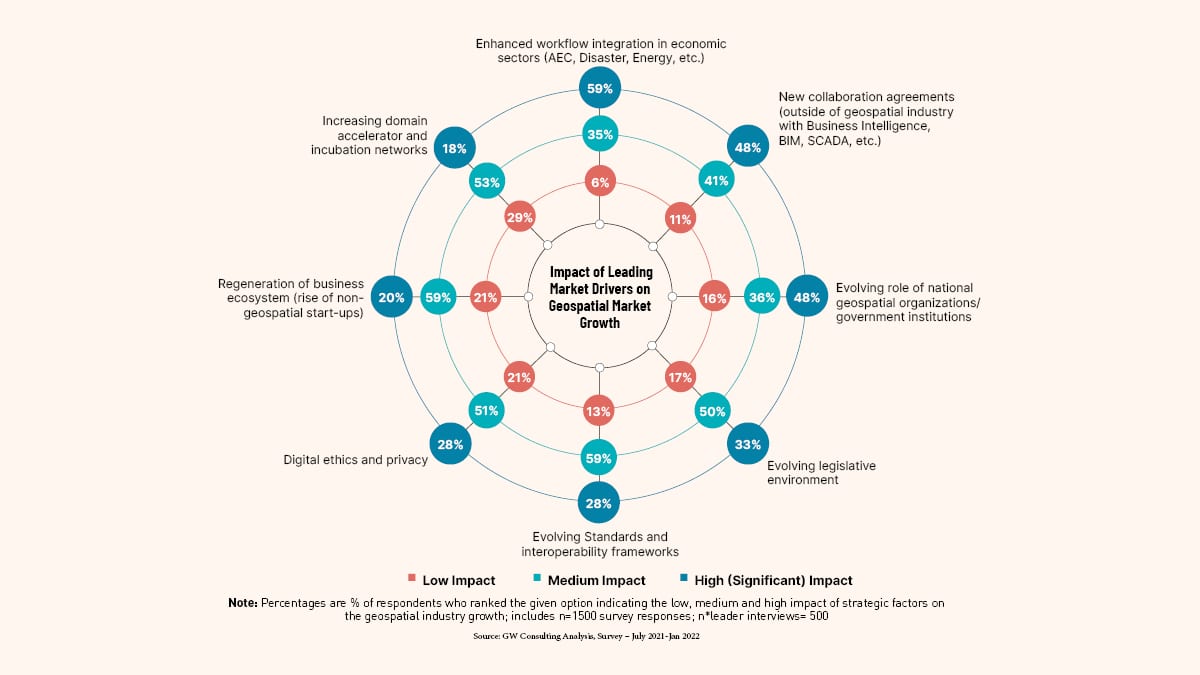

Source: GW Consulting Analysis, Survey – July 2021-Jan 2022

Public policy and market growth

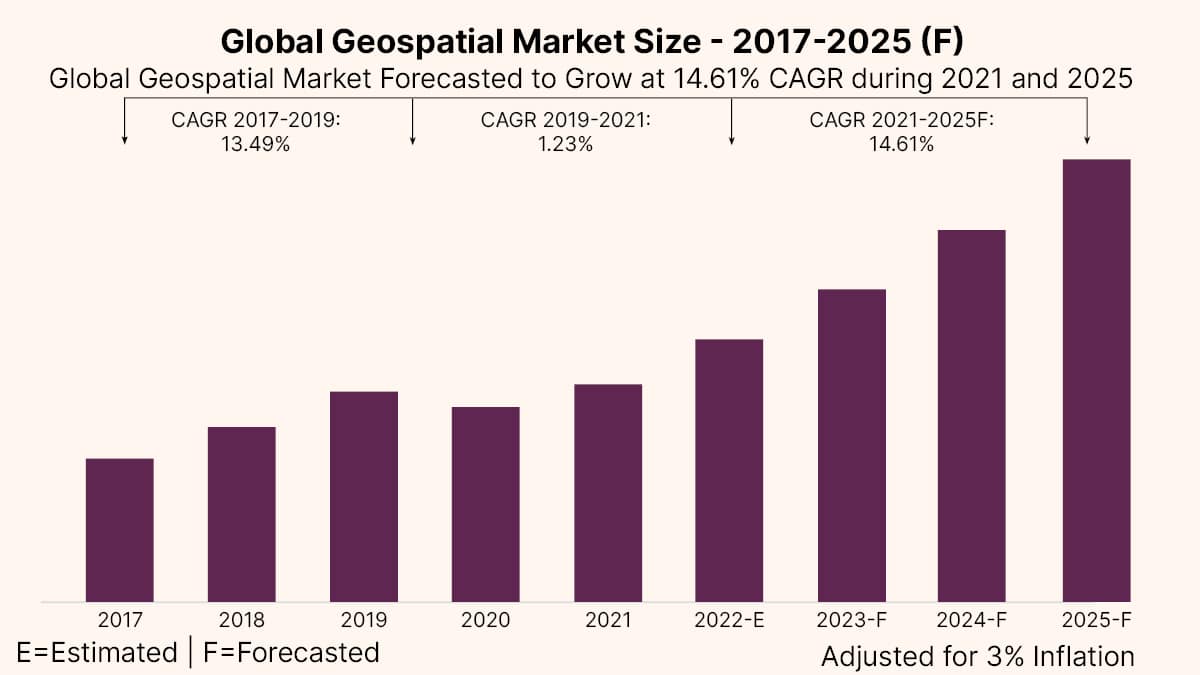

The Global Geospatial Market Size is estimated to be USD 452 billion in 2022 and is forecasted to grow at 14.61 percent CAGR and estimated to be USD 681 billion in year 2025.

However, it is expected to grow at much faster rate of 16.1 percent CAGR post 2025, reaching USD 1.44 trillion by 2030. While the current growth rate is driven by technology innovation, integration of workflows, and augmentation of spatial analytics in business processes, post 2025, this will gain momentum due to public policy reforms and increasing investments in geospatial infrastructure (both public and private) and industry acceleration programs worldwide. The growth impact of public policies and industrial acceleration is estimated to be USD 373 billion between 2025 to 2030 as compared to USD 38 billion in the year 2025, carving out a greater role for national geospatial agencies and governments.

GNSS and Positioning continues to be the largest and growing segment of geospatial market worldwide, accounting for almost 55 percent of the total market share, followed by spatial analytics at 25 percent, and Earth Observation at 17 percent. A decade ago, data was the biggest segment of geospatial market, but technology innovations in the field of software integrated hardware and integration of workflows have augmented analytics as a service, converting the market share of data to spatial enterprise and location-based services.

Source: GW Consulting Analysis, Survey – July 2021-Jan 2022

Hot spot for tech leadership

The geospatial market is emerging as a ‘hot spot’ of technology marketplace, wherein several mainstream IT and engineering firms added geospatial portfolios through strategic partnerships and acquisitions. The move is driven with motivation to add geospatial dimension to their existing business portfolios and preparing themselves to stay ahead of the innovation and competitive curves.

Key findings from the report include

The global geospatial market is forecasted to be USD 681 billion in 2025.

The market is estimated to grow at a much faster rate post-2025, making it USD 1.44 trillion by 2030, on the backbone of strategic public policy reforms, industry acceleration strategies, and innovations in the digital twin and metaverse paradigm.

The current growth in the market is driven by technology innovation, integration of workflows, and augmentation of spatial analytics in business processes.

Increasing government investments, strategic public policy reforms, and the evolving role of national geospatial agencies and governments is expected to drive the market growth post-2025.

GNSS and Positioning is forecasted to be the largest and growing geospatial technology segment with approx. 45 percent of the total market share, followed by GIS and Spatial Analytics at approx. 25 percent and earth observation at approx. 17 percent.

The economic impact of geospatial technologies on the global economy is currently estimated to be in the range of USD 2.2 trillion to 5.4 trillion, while it shall expand in the range of USD 5.4 trillion to USD 10.2 trillion in 2025.